Two founders, same October

Two founders open the same spreadsheet on the same Tuesday in October.

Their companies look almost identical from the outside. Similar product, similar traction, the same twelve weeks of runway left in the bank. Both have a list of two hundred investors someone told them was good. Both start sending the same kind of email.

By December, one has closed a round. The other is writing a layoff plan.

It is tempting to look for the difference in the obvious places. A better deck. A sharper email. A warmer market. None of these is the answer. The two companies were close enough at the starting line that the obvious variables cancel out. The difference was decided months earlier, in a stretch of time neither founder would have called "fundraising" while it was happening.

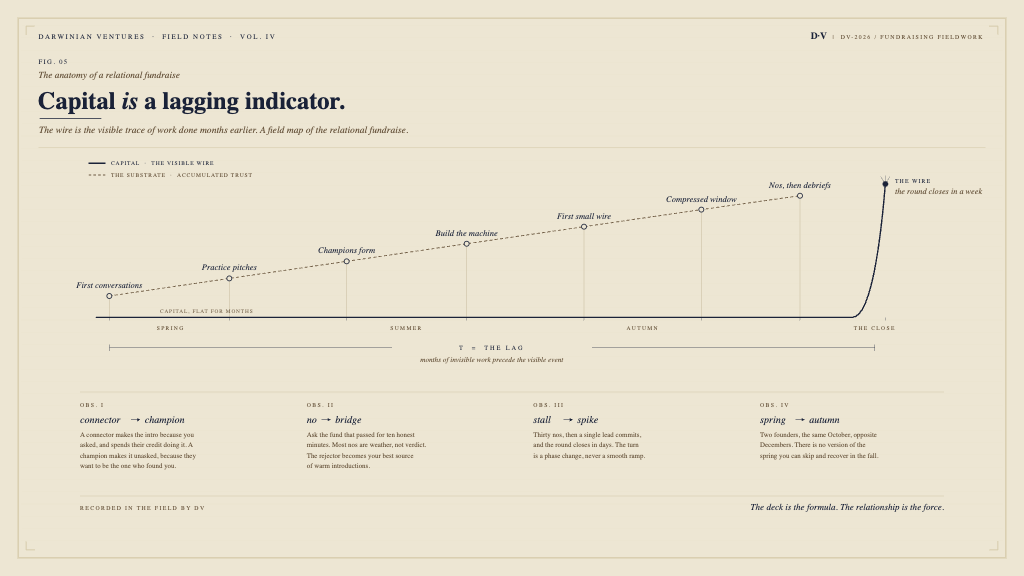

Capital is a lagging indicator.

The wire that lands in December looks like the result of the pitch that came right before it. Cause, then effect. It is almost never what actually happened. The wire is the visible end of a process that was mostly invisible and mostly slow: months of small interactions that built up, inside one person, enough trust to hand a near-stranger a large amount of money on badly incomplete information. The pitch meeting is where that trust got converted into a decision, not where it was built. By the time the founder walked into the room, the outcome was mostly set by whether the trust existed to be converted at all.

Most founders have the causality backwards. They believe the pitch produces the raise. It is closer to the final step of a process whose decisive work happened earlier, offstage, in conversations that did not feel like fundraising at the time.

We will come back to the two founders. First the mechanism, because everything follows from it.

Money moves at the speed of trust

Consider what you are asking an investor to do. You are asking a person who barely knows you to bet on you, in a market that may not exist yet, on a product that might not work, with money they cannot recover for ten years. By any normal standard this is insane, and the only thing that makes it rational is trust. That kind of trust does not assemble in thirty minutes. It assembles the way trust always does between two people: slowly, through repeated contact, through watching someone say they will do a thing and then do it, through whether the story they told in March still holds in June.

The founder who walks in cold is asking a stranger to manufacture, in half an hour, a confidence that normally takes months. Money moves at the speed of trust, and there is no setting on the dial that goes faster. Go looking for the faster setting and you find the version that burns relationships without producing checks: a well-connected friend, a request made too early.

The story we inherited is wrong

Part of why founders get the causality backwards is that the culture taught them to.

Open any founder podcast and the story has the same shape. Founder builds something remarkable, takes a meeting, investor sees the magic, term sheet by Friday, round oversubscribed and closed in two weeks. It gets told because it is a good story, because the people telling it have an interest in the version of reality where their fund is where lightning strikes, and because the founders who lived it prefer the lightning-strike memory to the truer, more boring one.

What it is, structurally, is survivorship bias. The fundraises that took eight months, with four near-misses and three rewrites of the narrative and a final term sheet below where the founder hoped, do not get told on podcasts. They survive in private memory and the occasional honest late-night conversation.

If you absorb the lightning strike as the baseline, you misjudge the whole shape of the work. You assume a fundraise is a short, hot event, so you start late, run fast, and panic when it does not resolve on the timeline you were promised. The honest baseline, for a first-time founder without unusual advantages, is months of relationship-building that does not feel like fundraising, then a concentrated window of meetings inside which a long string of nos accumulates before anything converts, then a sudden inflection. The lightning strike exists. It is not the median, and assuming it is yours is one of the more expensive assumptions a founder can make.

The four founders who get to skip the line

There are real exceptions, and the cost of mistaking yourself for one is measured in months of runway.

You can compress the timeline if you have specific, repeatable traction. Not "users are growing." A stranger who had to go to their own boss for budget, who bought for a reason you can articulate, in a pattern you can reproduce across the next hundred strangers. The dollar figure matters less than the repeatability. Investors are not paying for the revenue. They are paying for evidence the revenue is a machine and not an accident.

You can compress it if you have done this before. A founder who has taken a company to a real outcome starts the next one with investors who already know what it is like to back them. The trust this essay is about building, that founder built last time.

You can compress it if you carry real reputation into the raise. The early employee at a category-defining company, the researcher whose work is the technical heart of the company. The trust already accumulated, just under a different name, and it transfers.

And you can compress it if a credible investor approaches you first, unsolicited. Rare, and easy to overrate, because one interested investor is not yet a market. But there is a real buyer in the room before you have done any selling.

Notice what is not on that list. "We are early to the market" is not an advantage. Founders say it like a trump card. But being early is not a moat, and markets do not pay a premium for it. They reward evidence that a specific team will win a specific category.

There is a harder honesty worth saying, because it saves people years. Venture capital is a power-law business, built to underwrite outcomes that could become enormous. If your company is good, even very good, but is not, in its most optimistic honest projection, the kind that could return a fund on its own, then venture capital is the wrong instrument, and the raise will feel like rejection at every turn because it is a category error, not a verdict on you. The relational work amplifies a real opportunity. It cannot manufacture one that is not there.

If you are not one of those four founders, and the company is genuinely a venture bet, assume the median timeline is yours and the relational work is your job. The rest of this is how it is done.

The work that does not look like work

Return to the founder who closed in December. What was she doing in the spring?

She was having conversations with investors that were not pitches.

This distinction is the whole game and it is constantly misunderstood. She was not soft-pitching. Investors see the soft pitch coming from a long way off, and it casts the founder as seller and the investor as gatekeeper, the exact dynamic she wanted to avoid. She was actually asking for their read. She had a view forming about her market and genuinely wanted to know what experienced people saw that she did not. That curiosity cannot be faked over months, and investors, who spend their lives being pitched, can feel the difference between a founder who wants their money and one who wants their thinking. They relax around the second in a way they never do around the first.

There is a tactical layer founders violate even when they understand the principle: the first few minutes of those early conversations belonged to the investor. She asked about their firm, what they were seeing, why a thesis interested them. Investors are rarely invited to answer the questions they spend their days asking, and those minutes told her what each one actually cared about, more accurately than any research could. Only then did she talk about herself, letting the company emerge from her own story rather than arrive as a deck.

And she practiced, not in front of a mirror but in front of people. The practice pitch is one of the most underused tools in fundraising, because the name makes it sound optional. It is a meeting with someone who cannot write the lead check, an operator a level above her, a founder a stage ahead, in which she gave the real pitch and asked them to attack it.

How she ran them mattered. A practice pitch is not a slide review, not a conversation about whether slide three precedes slide four. That produces feedback at the wrong altitude and signals a low-stakes favor. She ran them as the real thing, because she wanted the other person to leave with the actual weight of the company in their head. When the weight lands, two things happen. She got a true read: the questions a sharp operator asks for real are the questions investors ask. And, the part almost no one anticipates, when the weight lands on someone who believes it, they start looking for ways to be associated with it. Some asked to put in a small check. Most did not. But many, unprompted, began introducing her, because they wanted to be the person who spotted it early.

Run correctly, the practice pitch does three jobs at once: it sharpens the pitch, rehearses the delivery, and manufactures advocates. The first few do none of this, but they are how the pitch becomes the pitch. By the eighth, the introductions arrived on their own. This is the texture of the work that does not look like work. Coffees that lead nowhere. Feedback she did not need. Pitches to people who could not fund her. None of it appeared on a calendar labeled fundraising. All of it was the fundraise.

The Taylor Swift problem

Now the move the other founder made, the one who waited until October, and why it quietly destroyed the thing she was trying to use.

Imagine you have a friend genuinely close with Taylor Swift. You decide you would like to meet Taylor, so you ask your friend for an introduction.

Sit with what you just did. Your friend spent years building that relationship, and you are asking them to spend some of it on someone Taylor has no reason to care about. Your friend knows many people who would also like to meet Taylor, and has learned that most have nothing she would find interesting, and that every introduction spends down a finite reserve of goodwill. So your friend hedges. If they make the introduction at all, it comes wrapped in protection: "not sure it's quite your thing, but he's a good guy." That hedge is the sound of someone shielding a relationship they value from a request they cannot fully stand behind.

The investor version is identical. When a founder asks a well-connected person for ten investor introductions, the favor gets spent before the founder has earned conviction. The recipient takes each meeting as a courtesy, not a verdict, and the founder spends it operating against the quiet context of being a favor. The investor passes, politely. Now the connector has less standing than before, filed slightly under "sends me mediocre deals," and the founder has degraded a relationship that was not theirs to spend, for one underpowered meeting. This is the most common way first-time founders destroy their single most valuable asset, and they do it believing they are being resourceful.

The founder who closed in December did the opposite, and it took longer, and there was no way to make it take less time. She made the connector excited first. She shared her thinking, asked for feedback, showed progress, gave the real pitch with real weight. Some decided to invest. Most did not. But once genuinely convinced, they did something a connector never does. They started volunteering introductions, unprompted, because they wanted to be associated with the thing.

The volunteered introduction is a different object. The recipient is not doing anyone a favor. The connector is not spending goodwill. They are showing someone they respect something they think that person will be glad to have seen, because excitement wants company. This is the difference between a connector and a champion. A connector makes the introduction because you asked. A champion makes it because they want to be the one who brought the deal in. You cannot ask someone to be a champion. You can only do the work that turns them into one.

One champion changes the math. Five champions, given a year, will out-produce fifty cold introductions sent in a panic, because they are talking about you in rooms you will never see, naming you to investors they respect months before you send an email. When you finally walk into those rooms, the partner is already half-convinced. You do not raise from strangers. You raise from people whose friends already told them about you.

Run it like a machine

Here is a strange thing about even disciplined founders. They run the product like a machine, and go-to-market like a machine: roadmap, pipeline, conversion rates, weekly review. Then they run the single most existential process in the company's life, the one that decides whether there is a next quarter, like a panic. Scattered emails, no tracking, no funnel, memory as the system of record. There is no defensible reason for it. A fundraise has every property of an operational function: inputs, a funnel, conversion rates, a deadline, an iteration loop. Run it like one.

The founder who closed built a spreadsheet, and it is more instructive than it sounds. One row per target investor, two hundred names from public lists, the cap tables of companies in her space, the portfolios of funds she admired, filtered fast on one question: do they invest at her stage, in her sector, in the last twelve months.

Then the column that did the real work. For each investor, the single person in her network most able to credibly introduce her. This cannot be delegated or automated, because who knows someone well enough for an introduction to mean something is a question only the founder can answer. It took days, and it was the difference between a list of strangers and a map of paths.

She tiered the targets and did something counterintuitive with the order: she started not with the funds she wanted most but with the tier she wanted least, the newer and hungrier funds, because her fortieth pitch would be far better than her fourth, and she refused to spend her best targets on her worst version of the pitch. Then she flipped the spreadsheet, the move almost no one makes alone, rebuilding it around connectors instead of investors: one row per person who could introduce her, and against each, every target they could reach. A small handful of people accounted for an outsized share of the paths. They were not strangers. They were people she could take to coffee with a real reason, and exactly the people whose practice pitches mattered most, because their conviction was the lever that opened the most doors.

Underneath ran a CRM, not optional and not sophisticated. Every conversation is data: the questions, the objections, the cadence, the source, the eventual yes or no. By the eighth investor, memory fails and you miss the pattern. The CRM is a diagnostic instrument: it tells you, in week three, that every pass comes from the same tier because you are pitching a Series A story with seed metrics, or that one objection keeps surfacing because part of the narrative is broken and can be fixed once. The founder running on hope never finds these patterns. The founder running a machine finds them while there is still time to act.

The machine protects one more thing: control of the timeline. Investors sensing a founder who is not running a process will run it for them, through requests each individually reasonable. A little more diligence. A reconnect next quarter. Granted in aggregate, they hand your timeline to a party whose incentives are not yours. When an investor says reconnect when you have more traction, the right move is usually to thank them, mark them a no, and move on. The fund that wants to back the company you are today is the right fund. The fund that wants to wait until you are a different company will, next quarter, want to wait again. The bus has a driver. The point of the machine is to make sure it is you.

The first small wire

Ten thousand dollars in the bank changes everything, and almost nothing.

It changes almost nothing about the runway. Twelve weeks becomes twelve weeks and a few days. But it changes the founder, because it changes the sentence. Before the first wire, every conversation contains a version of: "We are raising, we are talking to some great firms, we hope to start closing soon." After it: "We have closed our first investors, the round is in motion, another check came in last week." On the page nearly identical. In the room, different species. The first invites delay, because nothing is yet happening. The second creates urgency, because something is happening and the listener can feel it. The investor often cannot say why they are leaning in faster. They are leaning in faster anyway.

This is why advisor checks matter out of all proportion to their size. An advisor check is a small wire from someone who is not a traditional investor: an operator in the space, a founder a stage ahead, frequently the very people she ran practice pitches with, who got excited and wanted skin in the game. Ten thousand dollars, twenty-five thousand, sometimes on a slightly better cap as a thank-you for moving first. Immaterial to the total raised, decisive to the posture she carries into every subsequent room.

The mechanics make it clean. SAFE notes are unilateral. A founder can close anyone, at any time, at any cap, before a lead exists. Early believers come in low, the lead enters at a fair number, latecomers pay a premium for entering a round visibly hot. Everyone gets the terms appropriate to when they found the courage to commit. The first small wire is the bridge from raising to closing, and it comes from someone she had been talking to for months, which is to say it is, like everything else here, a lagging indicator.

The small wire pairs with a move founders routinely get backwards: the shape of the calendar. Spread meetings across whatever weeks investors happen to be free and you get separate, unhurried negotiations under no pressure to decide. Compress them into a tight window, two or three weeks in dense succession, and investors begin to sense one another, notice other firms looking, and the fear of missing out, the engine that actually converts early rounds, switches on. But the window only generates pressure if there is a market to compress, and that market is the relational substrate. It is not a trick you apply to a cold list. It is the visible spike on top of a ramp that took months to build.

What comes after no

For all of that, the first month of the meeting window will mostly produce nothing.

Some nos. Many polite delays. Several "come back when you have more traction." A partner who loved it and could not move the committee. Smart, experienced, credentialed people, looking the founder in the eye and telling her that the thing she has staked her career and savings and family's stability on is not worth their money or time.

No preparation makes this easier. Every founder who has run a real process has, at some point, sat in a parked car after a meeting and quietly wondered what they are doing with their life. The highlight reels do not include the parked car.

And here is the move almost no founder makes in that car, the single highest-return action in the entire fundraise. After a fund passes, she asked for a debrief. Ten minutes, the next afternoon, ideally to their cell. "I appreciated your time. I'd value hearing, briefly, how the conversation went on your side. What came up. What worked. What didn't."

Almost no one does this, and the reason is not strategic, it is emotional. Rejection is painful, and the instinct is to file the rejector away and never look again. Which is exactly backwards, because the fund that just passed is, for four reasons, one of the most valuable people she can call.

First, the reason for the no is usually not about her. The fund was near the end of its vehicle, or had a conflicting bet, or was quietly raising its next fund, or had used its allocation for the quarter. Every no feels like a verdict. The debrief reveals which are verdicts and which are weather, and most are weather, which returns the confidence she was about to spend on self-doubt.

Second, the fund liked her more than the polite email said. They took the meeting. Their real opinion is almost always warmer and more specific than the rejection let on.

Third, the act of asking converts her standing in their memory. Investors take five first meetings a day for years, and founders blur into one indistinct procession. The founder who circles back for a debrief steps out of it. She becomes the person who took a no with grace, who wanted to learn, who ran a process serious enough to extract value from a loss. Small in the moment, enormous across the years an investor spends remembering people.

Fourth, and most counterintuitive, the funds that passed will hand her some of the best introductions of the raise. The conventional advice says never take an introduction from someone who rejected you. It is wrong, because it misreads the emotional state of a fund that just passed. They feel slightly guilty, they want to be useful, and they hold real conviction about parts of the story they could not, for internal reasons, back with money. So they introduce her: to better-fit investors, to portfolio executives who might become customers, to operators who would make excellent advisors. These carry unusually high conviction, because they come from people who studied the company seriously and chose to advocate with no remaining stake. There are real fundraises where the bulk of the round traces back to introductions made by the funds that first said no. The no became the bridge to the lead. It costs ten minutes. Almost no one does it.

Then the round closes in a week

And then, somewhere in that grim flat stretch, the inflection comes.

One conversation converts. A lead emerges. A real check, a million and a half dollars, lands in writing. The CRM that had been filling in red for weeks begins, suddenly, to fill in green.

What happens next is not gradual. It is discontinuous, the most important and least understood feature of how rounds close. The stalled follow-ups accelerate. The investors who were hedging develop, overnight, a reason to move. The introductions she had stopped expecting arrive unbidden. The question in every room flips from "should I do this" to "do I still get to." The last seven hundred thousand closes inside a week, at a higher valuation than the lead came in at, for no reason other than that the lead came in. The round impossible for two months closes in three weeks.

The transition from impossible to inevitable is almost never a smooth ramp. It is a phase change. One credible commitment alters the structure of every remaining conversation at once, because it calls the market into existence, and once the market exists it forms fast. The flat month was not failure. The flat month was the substrate becoming visible.

Most founders try to skip the flat stretch and cannot. They panic and send more cold emails, optimizing a conversion rate that was never the bottleneck. The substrate is. When it is not built, the inflection never comes, the founder runs out of meetings before running out of runway, and concludes, in the parked car, that the market was bad or the deck was wrong. The market was usually fine. The deck was usually fine. The substrate had not been built.

Which returns us to the two founders in October. The one who closed did not have a better company or deck or luck. She spent the spring in rooms that did not feel like fundraising, building the trust the December wire turned out to be a lagging indicator of. The other spent those months heads-down on the product, which felt responsible and was, in every respect but the one that decided the outcome. Both worked brutally hard. Only one spent the work on the thing the wire trails behind.

Capital is a lagging indicator of relationship. The wire is the visible event. The relationship is the invisible cause, built slowly, months earlier, in small repeated interactions with people who were not, in the moment, being asked for anything.